Licensee for your personal loan: Boyledown Lending Inc.

Address of Licensee:

Boyledown Lending Inc.

285 Crockett Hill Lane, Cross Junction VA

david@boyledown.com

631-379-0306

This loan is made in compliance with the Consumer Financial Protection Bureau Regulation Z (12 C.F.R. Part 1026).

This disclosure is required by Virginia law (§ 6.2-1524(D)). At the time a loan is made, lenders must provide borrowers with identifying information about the parties to the loan and a standardized disclosure that complies with federal law (Regulation Z, 12 C.F.R. Part 1026).

In plain terms, this ensures you know exactly who you are borrowing from, who is responsible for the loan, and the key financial terms in a format designed to be clear and comparable across lenders.

This loan is made pursuant to Chapter 15 of Title 6.2 of the Code of Virginia

This language is required by Virginia law (§ 6.2-1524(K). We are legally obligated to include this exact statement in every loan agreement issued in Virginia subject to the Virginia Consumer Finance Law.

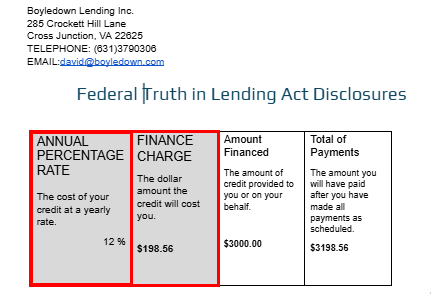

This disclosure is provided in accordance with federal Truth in Lending requirements under Regulation Z (12 C.F.R. Part 1026). The Annual Percentage Rate (APR) and Finance Charge are required to be presented in a clear and conspicuous manner because they represent key measures of the cost of credit.

The definitions and calculation methods for these terms are established by federal regulation and are applied consistently across covered credit transactions. This supports standardized disclosure and comparison of credit terms.

Federal regulations require that certain terms be presented clearly and conspicuously. The method used to satisfy this requirement may vary, provided that the terms are reasonably noticeable and understandable within the context of the disclosure.

The APR and Finance Charge are among the required key cost disclosures. These terms are presented in a highlighted format to support visibility within the disclosure document.

The regulations do not prescribe that these terms must be more prominent than the lender’s name or the heading identifying the disclosure as “Federal Truth in Lending Act Disclosures,” provided all required disclosures are presented in a clear and conspicuous manner.

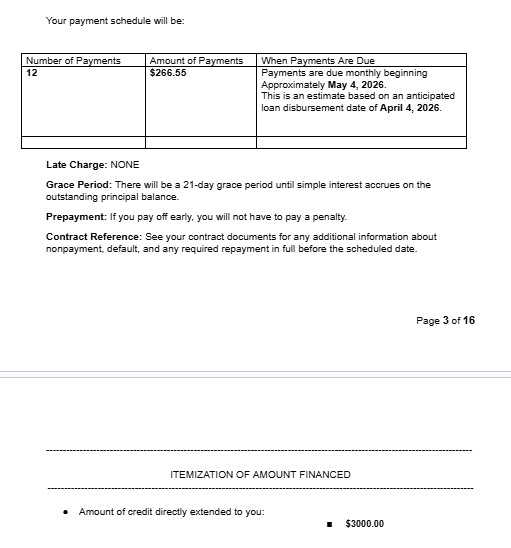

This section provides key details about how the loan is repaid, including the number of payments, the amount of each payment, when payments are due, and how late payments are handled. Some of these disclosures are required by law, while others reflect choices made by the lender.

We believe these details matter. For example, this agreement includes a clearly defined grace period, which is longer than what is commonly offered in the industry. We also do not charge late fees. These are intentional decisions designed to make repayment more predictable and fair.

This section may also include an itemization of the amount financed, showing where the loan proceeds are going and to whom. In simpler loans, this may just reflect funds disbursed directly to you. In more complex products—such as debt consolidation loans—this can include payments made directly to creditors on your behalf, which can make the breakdown more detailed.

Disbursement date = when the lender lets the money go

Loan Proceeds Receipt date = when the borrower actually gets the money

(Timing may vary depending on payment method)

Including the name and address of the principal debtor is required by Virginia law (§ 6.2-1524(D)). This ensures that the parties to the loan are clearly identified in the agreement.

Other information included in this section may not be strictly required by law but is collected to support internal recordkeeping and loan administration. This helps ensure accuracy in servicing the loan and maintaining proper documentation.

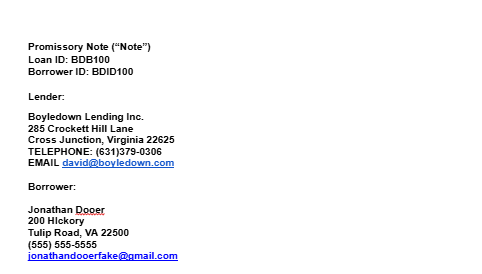

- Parties. For value received, Jonathan Dooer (“BORROWER”), residing at 200 Hickory

Tulip Road, VA 22500, promises to pay to the order of BOYLEDOWN Lending Inc. (“LENDER”), a Virginia-licensed consumer finance company, License No. CFI-256, the principal sum of $3000.00, together with simple interest at the rate of 12% per annum, accruing from the date funds are disbursed to BORROWER.

This section begins the loan contract and sets out the core terms of the agreement. It incorporates certain disclosures required by applicable federal and state law, which may appear either within this contract or in separate disclosure documents depending on legal requirements.

This provision identifies the parties to the agreement, states the principal amount of the loan, and sets forth the borrower’s promise to repay that amount with simple interest at the stated rate. These are fundamental terms required for the formation of the loan contract.

The structure and formatting of contract terms may vary within the bounds of applicable law and regulatory requirements. The presentation of information in this document is intended to organize required terms in a clear and readable format for reference.

Principal means the total loan amount stated in this Note. It is the amount the Borrower is obligated to repay under the terms of the loan, excluding separately stated interest and fees.

Disbursement (or “Net Proceeds”) means the amount of loan funds actually received by Borrower at the time of funding.

The Principal Amount and the Disbursement Amount may differ depending on how any fees are applied in connection with the loan.

1. Origination Fee Deducted at Funding

If an origination fee is deducted from loan proceeds at or prior to funding, the Principal Amount remains the full amount stated in this Note, while the Disbursement is reduced by the amount of the fee.

Example:

Principal: $10,000

Origination Fee: $500

Net Disbursement: $9,500

2. Origination Fee Included in Principal

If an origination fee is included in the Principal Amount, the total Principal increases by the amount of the fee, and the Borrower receives the full stated loan proceeds.

Example:

Original Loan Amount: $10,000

Origination Fee Included: $500

Principal Amount: $10,500

Net Disbursement: $10,000

Summary

The Principal Amount is the contractual loan balance used to determine repayment obligations. The Disbursement Amount reflects the actual funds received by Borrower at funding, which may differ from Principal depending on fee structure.

2. Conditional Nature of Agreement. BORROWER acknowledges and agrees that submission of a loan application and this signed Note does not obligate LENDER to make a loan. BORROWER is not bound by the terms of this Note unless and until LENDER disburses loan funds to BORROWER.

This provision describes the conditional nature of the loan agreement. Submission of a loan application and execution of the promissory note do not, by themselves, create an obligation for the lender to fund the loan.

The lender’s obligation to disburse funds arises only upon actual funding of the loan. Until loan proceeds are disbursed to the borrower, the agreement does not become effective as a funded loan transaction.

This structure reflects the distinction between the application and approval process and the consummation of the loan, which occurs at the time funds are disbursed.

3. Binding Effect Upon Funding. Upon funding of the loan by LENDER, BORROWER agrees that this Note shall constitute a legally binding agreement, and BORROWER shall be obligated to repay the principal and interest in accordance with the terms herein.

This provision explains when the loan agreement becomes legally binding. Upon funding of the loan, the promissory note becomes an enforceable contract between the borrower and the lender.

Once the agreement is effective, both parties are obligated to follow its terms. The borrower is required to repay the principal and interest in accordance with the repayment terms set out in the agreement.

If the borrower does not comply with the repayment obligations after the loan is funded, the agreement may be enforced through available legal processes.

4. Payments.

(a) Payments. This Note is payable in 12 equal monthly installments, each consisting of principal and interest. Interest begins to accrue on the date of disbursement. The first payment is due on May 4, 2026, and subsequent payments are due on the same day of each month thereafter until the final payment date of April 4, 2027, which is the maturity date of this Note.

This loan is structured as a level payment amortizing installment loan. The borrower makes equal monthly payments over a fixed term, and each payment is applied to both principal and interest.

Interest accrues on the outstanding principal balance from the date of disbursement. As payments are made, the portion applied to principal increases over time while the portion applied to interest decreases.

This results in a gradual reduction of the outstanding balance until it reaches zero at the final scheduled payment date.

(b) Due Dates Falling on Irregular Days. If a regularly scheduled due date falls on the 29th, 30th, or 31st of a month that does not include that day, the payment shall instead be due on the last day of that month unless otherwise agreed in writing.

This provision ensures that payment due dates remain consistent in months with fewer calendar days. If a scheduled due date does not exist in a given month, the payment is automatically moved to the last day of that month.

Where the loan includes a grace period (for example, a 21-day grace period), the grace period is calculated from the applicable due date as adjusted under this provision. The length of the grace period remains fixed; however, the calendar end date shifts depending on the number of days in the applicable month.

Example:

If a payment is due on January 31, the due date in February becomes February 28 (or February 29 in a leap year). A 21-day grace period would run from the adjusted due date. As a result:

• Non-leap year: February 28 + 21 days = March 21 payment deadline

• Leap year: February 29 + 21 days = March 21 payment deadline

By contrast, in a 31-day month (such as March), the due date remains March 31, and the 21-day grace period extends to April 21.

(c) Application of Payments. Each payment received will be applied first to any accrued and unpaid interest, then to the outstanding principal balance, and finally to any other amounts owed under this Note, including reasonable costs of collection or attorney’s fees if applicable. No unpaid interest or charges will be capitalized into principal.

This provision sets the order in which payments are applied, commonly referred to as the “payment waterfall.” Payments received are applied first to accrued and unpaid interest, then to outstanding principal, and finally to any other amounts owed under the Note, such as collection costs or attorney’s fees if applicable.

This allocation method is standard in installment lending and reflects the structure of an amortizing loan, where interest accrues over time on the outstanding principal balance. As a result, early payments are generally applied more toward interest than principal, with the proportion applied to principal increasing over time as the balance declines.

This provision also clarifies that unpaid interest and charges are not capitalized into principal, meaning interest does not become part of the principal balance unless expressly stated elsewhere in the agreement. This prevents unpaid interest from compounding into the loan balance.

(d) Overpayments. Any payment received in excess of the amount then due shall be credited toward the Borrower’s next scheduled payment unless the Borrower requests in writing that such excess be applied directly to reduce the outstanding principal balance.

This provision governs how payments in excess of the amount currently due are applied under the Note. By default, any overpayment is applied to the next scheduled installment unless Borrower provides written instructions to apply such excess directly to the outstanding principal balance.

Application of an overpayment to a future installment may advance the due date of the next required payment. This approach affects payment timing but does not immediately reduce the principal balance on which interest accrues.

If Borrower elects to apply the overpayment to principal, the outstanding balance is reduced at the time the payment is received. This may decrease the total amount of interest accrued over the term of the loan and may affect the final payment amount or loan duration. Application to principal does not alter the due date or amount of the next scheduled installment unless otherwise agreed in writing.

Borrower instructions regarding the application of overpayments must be provided in writing.

5. Interest

(a) Accrual of Interest

- Interest on this Note accrues daily on the unpaid principal balance at the rate of twelve percent (12%) per annum simple interest, until the full principal is paid.

- If a scheduled payment is received within twenty-one (21) days after its due date, no additional interest will accrue beyond what would have accrued as if the payment were made on the due date.

- Payments received after the 21-day grace period will accrue interest from the original due date until paid in full.

Simple interest is calculated only on the unpaid principal balance. It does not accrue interest on previously accumulated interest. Interest continues to be calculated on the original outstanding principal until it is repaid.

Example (Simple Interest):

Loan: $10,000 at 12% per year

Interest each year: $1,200 (12% of $10,000)

Even as payments are made, interest is always based only on the remaining principal balance.

Compound interest is calculated on both the principal and any previously accrued interest. This means interest can generate additional interest over time, increasing the total cost of borrowing compared to simple interest.

Key Difference:

Simple interest does not charge interest on interest. Compound interest does.

(b) Effect on Final Payment

- Due to late payments, early payments, or rounding, BORROWER’S final payment may be more or less than the regular payment.

- BORROWER acknowledges that payments made after their scheduled due dates (and outside the 21-day grace period) may alter the amortization schedule, potentially resulting in a higher final payment.

(c) Interest Rate During Delinquency or Default

- The annual interest rate of twelve percent (12%) will remain in effect regardless of delinquency or default, unless modified by law or written agreement.

(d) Charge-Offs

- LENDER will generally charge off loans six (6) months after the maturity date, as originally scheduled or as extended under an approved deferment.

- Forbearance periods do not extend the maturity date unless expressly agreed in writing.

- Once a loan is charged off, interest will cease to accrue; however, BORROWER remains responsible for repaying the outstanding principal balance.

This provision reflects standard accounting and regulatory practices applicable to consumer lenders. Under U.S. generally accepted accounting principles (GAAP) and supervisory guidance, loans that remain delinquent for an extended period are typically required to be charged off for financial reporting purposes.

In general, closed-end consumer loans are charged off after reaching a specified level of delinquency, commonly measured as a period following the contractual maturity date or extended maturity date (if a deferment has been formally approved). This treatment is intended to ensure that a lender’s financial statements accurately reflect the collectability of outstanding loans.

Regulatory expectations related to safety and soundness also require lenders to recognize and address credit losses in a timely manner. Charging off a loan does not extinguish the Borrower’s repayment obligation; rather, it is an accounting action that reflects the loan’s status for reporting purposes while collection efforts may continue.

This provision clarifies that any period of forbearance does not, by itself, extend the maturity date of the loan. During a forbearance period, scheduled payments may be reduced or temporarily suspended; however, the original repayment timeline remains in effect unless the parties agree in writing to modify the loan terms.

As a result, any amounts not paid during a forbearance period may need to be repaid within the remaining term of the loan, which may affect the amount of subsequent payments or the final payment due.

This differs from a deferment structure, in which missed payments are typically added to the end of the loan term and the maturity date is extended accordingly.

This provision refers to interest under the loan agreement. If the loan is charged off, interest under the terms of this Note will no longer accrue. However, if the account is later subject to a court judgment, applicable law may provide for interest to accrue on the judgment amount from the date of judgment until paid.

6. Fees.

(a) There are no late payment fees for this loan.

(b) Attorney’s Fees.

In the event of litigation, the prevailing party is entitled to recover reasonable attorney’s fees and court costs.

7. Members of the armed forces: Federal law provides important protections to members of the armed forces and their dependents relating to the extension of consumer credit. In general, the cost of consumer credit to a member of the Armed Forces and his or her dependent(s) may not exceed an annual percentage rate of 36 percent. This rate must include, as applicable to the credit transaction or account: the costs associated with credit insurance premiums, fees for ancillary products sold in connection with the credit transaction; any application fee charged (other than certain application fees for specified credit transactions or accounts); and any participation fee charged (other than certain participation fees for a credit card account). Your payment obligation is shown on the Truth in Lending disclosure. Please call (631)379-0306 toll free to have the disclosure provided to you orally.

8. Proceeds. I agree that the proceeds of my loan will be paid via ACH payment delivered to BORROWER at closing, or in such a manner as LENDER determines. BORROWER acknowledges that the timeliness of crediting loan proceeds is dependent on the accuracy of the information BORROWER provides when BORROWER completes all loan origination activities, and the prompt crediting by the financial institution that holds BORROWER’S account. LENDER is not responsible for the action of the financial institution that holds BORROWER’S account.

9. Method of payment. BORROWER agrees to pay the principal, periodic interest and any fees on this note when due. LENDER has given BORROWER the choice of making BORROWER’S monthly payments by i) Zelle ii) ACH payment or iii) by personal check delivered by regular mail to,

BOYLEDOWN Lending Inc.

285 Crockett Hill Lane

Cross Junction, VA 22625

All written communications concerning disputed amounts, including any check or other payment instrument that (i) is postdated and accompanied by adequate notice, (ii) indicates that the payment constitutes “payment in full” of the amount owed iii) is tendered with other conditions or limitation or iv) is otherwise tendered as full satisfaction of a disputed amount must be marked for special handling and mailed or delivered to BOYLEDOWN Inc. at

BOYLEDOWN Lending Inc.

285 Crockett Hill Lane

Cross Junction, VA 22625

10. Waiver of Defenses. Except as otherwise provided in this Note or as required by applicable law, LENDER is not responsible or liable to BORROWER for the quality, safety, legality or any other aspect of any property or services purchased with the proceeds of BORROWER’S loan. If the BORROWER has a dispute with any person from whom BORROWER has purchased property, BORROWER agrees to settle the dispute directly with that person. Notwithstanding the foregoing, this section shall not apply if I am a “covered borrower” under the Military Lending Act, 10 U.S.C. section 987, and this section would waive a right to legal recourse that I have under federal, state, or other applicable law.

11. CERTIFICATION. Unless BORROWER has certified to LENDER otherwise, BORROWER agrees that the proceeds of this loan will not be applied (i) in whole or in part to postsecondary educational expenses (i.e., tuition, fees, required equipment or supplies, room and board, or other miscellaneous personal expenses) incurred while BORROWER is studying at a college, university, or vocational school, as the term “postsecondary educational expenses” is defined in Regulation Z, 12 CFR § 1026.46(b)(3); (ii) for any home purchase or refinance; (iii) for the purchase, sale, or transfer of firearms, ammunition, or related accessories; or (iv) for gambling purposes, including but not limited to wagering, betting, or the purchase of lottery tickets or gaming chips.

This provision requires Borrower to confirm the intended use of loan proceeds. Lenders may be subject to different legal requirements, underwriting standards, and regulatory frameworks depending on how a loan is used. As a result, certain uses of funds may be restricted or require the loan to be originated under a different product type or disclosure regime.

For example, loans used for postsecondary educational expenses, residential real estate transactions, or other regulated purposes may be subject to separate federal or state laws, including specific disclosure, underwriting, or licensing requirements. This certification helps ensure that the loan is originated and administered in accordance with the applicable legal framework.

In addition, lenders may impose internal policies limiting the use of proceeds for certain activities as part of their risk management practices. By obtaining this certification, the lender documents the intended use of funds at the time of origination and relies on that representation in making the loan.

12. Default, Remedies, Acceleration.

(a)Events of Default.

Subject to applicable state law and any required notice or cure rights, BORROWER will be in default under this Note (each, an “Event of Default”) if any of the following occurs:

- Payment Default. BORROWER fails to pay any amount due under this Note within six (6) months after the payment due date.

- Other Early Triggers for Default (Optional for Commercial Reasonableness)

LENDER may also deem an Event of Default to have occurred before six months if commercially reasonable standards indicate that BORROWER’s ability or intent to repay has been materially impaired, including but not limited to:

- abandonment of contact or refusal to pay;

- any other material breach related to repayment.

- Bankruptcy or Assignment. BORROWER files, or has filed against them, any bankruptcy or insolvency proceeding, or makes an assignment for the benefit of creditors.

- Death. BORROWER dies.

- Fraud or Misrepresentation. BORROWER commits fraud or makes any material misrepresentation in connection with this Note or the loan application.

- Other Material Breach. BORROWER fails to comply with any other material term of this Note.

This provision distinguishes between a missed payment and a refusal to pay. A failure to make a scheduled payment may occur for a variety of reasons, including timing or temporary financial constraints, and constitutes a payment default under the terms of the Note.

A refusal to pay, by contrast, involves a statement or conduct indicating that Borrower does not intend to satisfy the repayment obligation. This represents a more definitive indication of non-performance and may be treated differently for purposes of default classification and enforcement, subject to applicable law.

This provision also includes abandonment of contact, which may indicate that Borrower is no longer engaged in the repayment process. These conditions are identified separately because they may reflect a higher level of risk than an isolated missed payment.

This provision identifies the filing of a bankruptcy or insolvency proceeding as an event of default under the Note. The inclusion of bankruptcy as a default does not override or limit any protections available to Borrower under applicable bankruptcy law.

Instead, this provision establishes that a bankruptcy filing constitutes a default for purposes of the agreement. Following such an event, the rights and remedies of Lender are subject to the requirements and limitations imposed by the bankruptcy process, including any applicable automatic stay or discharge provisions.

This classification also allows the loan to be treated as in default for contractual, operational, and accounting purposes, and enables Lender to assert its rights within the bankruptcy proceeding as permitted by law.

(b) Delinquency

A payment not received within twenty-one (21) days of its due date will be considered delinquent, but will not automatically place the loan in default. For avoidance of doubt, a payment that is delinquent does not, by itself, constitute an “EVENT OF DEFAULT.” During this 21-day grace period, no additional interest will accrue on the missed payment.

(c) Acceleration and Remedies.

Upon the occurrence of an Event of Default, and subject to any notice or cure rights required by law, LENDER may declare the entire unpaid principal balance, together with all accrued interest, immediately due and payable (“Acceleration”). This right of acceleration is in addition to, and not in limitation of, any other remedies available to LENDER under this Note or applicable law, including but not limited to

(i) pursuing collection or legal action to recover the indebtedness;

(ii) recovering reasonable costs of collection, including attorney’s fees and court costs, to the extent permitted by law.

13. Prepayments; Partial Payments. BORROWER may prepay this Note in full or in part at any time provided BORROWER is current on all scheduled installments. Any partial prepayment will be applied first to any accrued interest, then to the outstanding principal balance. A partial prepayment will reduce the total interest paid over the life of the loan but will not postpone or satisfy any scheduled installment, unless LENDER agrees otherwise in writing. No prepayment penalty, fee, or additional interest will be charged for any full or partial prepayment made in accordance with this section. For the avoidance of doubt, regularly scheduled monthly payments made in accordance with the payment schedule are not considered prepayments. BORROWER must continue to make all regularly scheduled payments in the amounts and on the dates required until the entire indebtedness is paid in full.

14. Deferment and Forbearance

(a) Deferment

BORROWER may request a deferment in accordance with LENDER’s reasonable procedures. Approval is at LENDER’s sole discretion. During any approved deferment:

- Scheduled payments of principal and interest may be postponed, and the maturity date may be extended;

- Interest continues to accrue unless otherwise provided in writing by LENDER.

For the avoidance of doubt, an approved deferment temporarily modifies the payment schedule and may extend the maturity date but does not permanently change the underlying terms of the loan, including the principal balance, interest rate, or other obligations. Deferment may increase the amount of future payments or extend the repayment term, unless prohibited by law.

(b) Forbearance

BORROWER may request forbearance in accordance with LENDER’s reasonable procedures. Approval is at LENDER’s sole discretion. During any approved forbearance:

- Scheduled payments of principal and interest may be temporarily suspended or reduced, to the extent permitted by law;

- Interest continues to accrue unless otherwise provided in writing by LENDER.

Forbearance may increase the amount of future payments and, in limited cases, may extend the repayment term, unless prohibited by law. Forbearance does not permanently change the underlying terms of the loan.

Definitions

For purposes of this Note:

- “Deferment” means a temporary postponement of scheduled payments that extends the loan’s maturity date.

- “Forbearance” means a temporary suspension or reduction of scheduled payments without extending the loan’s maturity date, which may result in larger remaining payments to repay the loan by the original maturity date.

This section defines the terms “deferment” and “forbearance,” which are not uniformly defined in consumer loan agreements and may not be offered by all lenders. These terms are often used interchangeably in practice, but they may have different effects on payment obligations, interest accrual, and the loan term depending on how they are implemented.

By including definitions, this provision clarifies how each form of payment relief operates under this Note, including whether payments are postponed or reduced, whether interest continues to accrue, and whether the maturity date may be extended. This reduces ambiguity regarding how temporary payment accommodations affect the loan.

This section also establishes that any deferment or forbearance is subject to Lender approval and constitutes a temporary modification of payment obligations rather than a permanent change to the underlying loan terms, unless otherwise agreed in writing.

15. Waivers. Even if, at a time when BORROWER is in default, LENDER does not require BORROWER to pay immediately in full, LENDER will still have the right to require BORROWER to pay immediately in full if BORROWER is in default at a later time. Neither LENDER’s failure to exercise any of LENDER’S rights, nor BORROWER’S delay in enforcing or exercising any of BORROWER’S rights, will waive those rights. Furthermore, if LENDER waives any right under this Note on one occasion, that waiver will not operate as a waiver to any other occasion. Subject to applicable laws, unless BORROWER is a “covered borrower” under the Military Lending Act, 10 U.S.C. section 987, BORROWER waives presentment, notice of dishonor, protest and all other demands and notices in connection with the delivery, acceptance, performance or enforcement of this Note.

16. No Assignment by Borrower. BORROWER is not allowed to assign any of BORROWER’S obligation under this Note without LENDER’S express written permission.

17. Electronic Communications Consent

(a) Borrower consents to receive all communications, disclosures, notices, agreements, and other information (“Communications”) from Lender electronically in connection with this Note and any servicing, administration, or collection activity.

Borrower agrees that Lender may provide Communications by:

- email to the email address provided by Borrower, which is {{BorrowerEmail}}

- text message to any mobile number provided by Borrower, and

- posting to Lender’s online servicing platform (including BOYLEDOWN.com or any successor platform).

Borrower agrees that electronic Communications satisfy any legal requirement that such Communications be provided in writing, to the extent permitted by applicable law.

(b) Consent to Telephone and Text Communications

Borrower expressly consents to be contacted by Lender at any telephone number provided by Borrower, including mobile numbers, even if such number is reassigned or ported.

Borrower agrees that such communications may include:

- servicing communications,

- account updates,

- payment reminders, and

- collections-related communications.

Borrower further consents that Lender may use automated telephone dialing systems, prerecorded messages, or artificial voice messages, to the extent permitted by applicable law.

Borrower represents that Borrower is the subscriber or customary user of any telephone number provided and has authority to provide this consent.

(c) Permitted Methods of Communication

Lender may communicate with Borrower using any reasonable method, including:

- telephone calls (mobile and landline),

- SMS/text messaging,

- email,

- postal mail, and

- secure online portal messaging.

Communications may include sensitive account, servicing, and collections-related information.

This provision is intentionally broad to define the permitted channels for account-related communications and to distinguish them from public-facing platforms such as social media. Even where social media platforms offer private messaging features, they are not treated as reliable or secure channels for servicing or collections communications due to risks involving account access uncertainty, message visibility limitations, third-party platform control, and lack of consistent delivery or identity verification. Accordingly, borrower communications are limited to direct, verifiable methods such as phone, SMS, email, postal mail, and secure portal messaging to ensure privacy, compliance, and reliable receipt.

(d) Limits and Required Communications

Borrower may request that Lender limit certain non-essential communication methods; however, Borrower acknowledges that Lender may continue to send legally required notices and communications necessary to service, enforce, or administer this Note.

Borrower may update contact information at any time by notifying Lender through Lender’s designated communication channels.

(e) Methods BORROWER can contact LENDER

BORROWER can contact LENDR by visiting www.BOYLEDOWN.com and submitting a complaint or inquiry. BORROWER may also contact LENDER by emailing david@boyledown.com, by calling (631) 379-0306 during LENDER operating hours 9:00 AM –5:00 PM Eastern Standard time, each Monday through Friday that are business days, or by writing via regular mail to:

BOYLEDOWN Lending Inc.

Loan Operations

285 Crockett Hill Lane

Cross Junction, VA 22625.

18. Governing Law; Misc., BORROWER understands and agrees that LENDER is a consumer finance company licensed by the Virginia State Corporation Commission, with Consumer Finance Company License No. CFI-256. LENDER is located in Virginia. Consequently, the provisions of this note will be governed by the laws of the state of Virginia, to the extent not preempted by federal law, without regard to conflict of law rules. Without limiting the foregoing, all terms of this Note relating to interest, as that term is defined under applicable state law, shall be governed by Chapter 15 of the Code of Virginia. Section 16 (Arbitration Agreement) is governed by the Federal Arbitration Act, and not by any state law concerning arbitration. If any provision of this Note cannot be enforced, the rest of the provisions of this Note will stay in effect. No amendment of this Note will be valid unless in writing and signed by both LENDER and BORROWER. The Note represents the full agreement between LENDER and BORROWER regarding the BORROWER’S LOAN.

19. Complaints, Disputes, Arbitration.

NOTICE: IF THE BORROWER IS A COVERED BORROWER UNDER THE MILITARY LENDING ACT, 10 U.S.C. SECTION 987, THE FOLLOWING ARBITRATION AGREEMENT BETWEEN BORROWER AND LENDER DOES NOT APPLY.

(a) Governing Law. I acknowledge and agree that this arbitration clause will be construed and governed by the Federal Arbitration Act, 9 U.S.C., Section 1 et. Seq., (FAA) as amended. The Arbitrator (defined below) shall apply applicable law and applicable statutes of limitations consistent with the FAA and shall honor claims of privilege recognized by law.

(b) Dispute. “Dispute” means any action, dispute, claim, or controversy of any kind arising out of, in connection with or in any way related, even indirectly, to the Note or the extension of credit set forth in the Note. For example, “Dispute” includes claims related to: any relationship resulting from, or activities connected to this Note, my application, information I have provided to you, information and disclosures LENDER has provided to BORROWER, any prior agreements between BORROWER and LENDER, extensions, renewals, refinancings, payment plans, underwriting, servicing, collections, privacy, and customer information. The term ‘Dispute’ also includes claims under the federal or state consumer protection laws; claims in tort or contract, claims under statutes or common law, claims at law or in equity; other past, present and future claims, counterclaims, cross-claims, third party claims, interpleaders or otherwise, and any claim relating to the interpretation, applicability, enforceability or formation of this arbitration clause, including, any claim that all or part of this arbitration clause, except paragraph G below, is void, voidable or unconscionable.

(c) Mandatory Arbitration. Unless otherwise stated in this arbitration clause, any dispute between the Parties shall, at LENDER’S or BORROWER’S election or the election of any of our respective heirs, successors, assignees or related third parties, including any other subsequent holder of this Note, and their affiliates, subsidiaries, and parents, (the “Parties”), be resolved by a neutral, binding arbitration, and not by a court of law. This procedure includes any dispute over the interpretation, scope, or validity of this Note, this arbitration clause or the arbitrability of any issue, with the sole exception of the Parties; waiver of any right to bring a class action or to participate in a class action as provided for under paragraph G below shall be solely determined by the appropriate court, if necessary. This arbitration clause applies to the Parties, including their respective employees or agents, as to all matters which arise out of or relate to this Note or are in any way connected with the extension of credit set forth in this Note, or any resulting transaction or relationship.

(d) Facts About Arbitration. In arbitration, a neutral third party (“Arbitrator”) resolves Disputes, instead of a judge or jury. LENDER, with BORROWER, waive the right to go to court. The arbitrator will conduct a hearing, which is private and less formal than a court trial. Each side will have the opportunity to present some evidence to the Arbitrator. The Arbitrator may limit the Parties’ ability to conduct fact-finding prior to the hearing, called “discovery.” Other rights that the Parties might have in court might not be available in arbitration. Following the hearing, the Arbitrator will issue an award. The Arbitrator’s decision is final, and a court may then enforce the award like a court judgment. Courts rarely overturn an Arbitrator’s award.

(e) Pre-Arbitration Resolution. Prior to starting arbitration, BORROWER can call LENDER at (631)379-0306 or write to LENDER at:

Boyledown Lending Inc.

285 Crockett Hill Lane

Cross Junction, VA 22625

Or, BORROWER can email david@boyledown.com to attempt to resolve the Dispute. LENDER and BORROWER will attempt to resolve the Dispute. If LENDER makes a written offer (“Settlement Offer”) BORROWER may reject it and arbitrate. If we do not resolve the Dispute, either party may start Arbitration. No party will disclose settlement proposals, including a Settlement Offer, to the Arbitrator.

(f) Rules and Procedure. Either party may start arbitration by mailing a notice of arbitration, even if a lawsuit has been filed. Such notice shall be given by certified mail, return receipt requested. Notice to assignees or related third parties shall be sent to LENDER at:

Boyledown Lending Inc.

285 Crockett Hill Lane

Cross Junction, VA 22625.

The Party initiating the arbitration shall set forth in the notice the nature and factual basis of the Dispute, the names and addresses of all other parties, the amount involved, and the specific relief requested. The Responding Party must mail a response within 45 days, and may also set forth any counter-disputes. The American Arbitration Association (“AAA”) shall conduct any arbitration according to this arbitration clause. The AAA arbitration rules in effect when the claim is filed apply (“AAA Rules”), except where those rules conflict with this Arbitration Clause or any of LENDER’s agreements with BORROWER. BORROWER can get copies of the AAA Rules at the AAA’s website (www.adr.org) or by calling 800-778-7879. LENDER or BORROWER may choose to have a hearing, appear at any hearing by phone or other electronic means, and/or be represented by counsel.

(g) Class Action Waiver. The Parties agree to give up any right they may have to bring a class action lawsuit or class arbitration, or to participate in either as a claimant. The Parties agree to give up any right to consolidate or join any arbitration proceedings with the arbitration of others. The Parties give up the right to serve as a private attorney general in any jurisdiction in which such procedure might be permitted. To the extent the Parties are permitted to file small claims under paragraph K below the Parties agree that any small claim may only be brought on an individual basis and that no small claim may be brought on a class or representative basis. The parties further agree that if a court or arbitrator decides this Paragraph G is void or unenforceable, the arbitration clause shall be void and without effect.

(h) Fees and Costs: If BORROWER requests, LENDER shall advance all of the Arbitrator’s fees and expenses, as well as all administrative and filing fees, up to an amount of $1000. The Parties shall be responsible for their own attorneys’ fees associated with any arbitration, unless otherwise allowed under applicable substantive law and awarded by the Arbitrator. If the Arbitrator awards the funds, BORROWER will not have to reimburse any arbitration fees and expenses you have advanced. Any such reimbursement shall not exceed the filing fees and costs BORROWER would have incurred had BORROWER filed a lawsuit in a court.

(i) Exceptions. The Parties agree that this arbitration clause is not applicable to “small claims” meaning those claims that either Party is entitled to file and maintain in an appropriate small claims court or any action where the total amount in controversy is no greater than $10,000, including any claims for attorney’s fees and non-monetary relief. The Parties agree that any appeal from a judgment obtained pursuant to this paragraph shall be applicable only by arbitration according to the procedures set forth in this arbitration clause.

This provision is a limited exception to the general arbitration requirement. While arbitration clauses are commonly used in consumer lending agreements to establish a uniform dispute resolution process, they are typically not intended to displace a party’s ability to resolve very small disputes in small claims court.

The “small claims” exception allows either party to pursue claims within a limited monetary threshold (here, up to $10,000) in an appropriate small claims court. This is intended to provide a faster, lower-cost forum for resolving minor disputes without engaging in the full arbitration process.

For small-dollar lending arrangements, this type of carve-out is often used to preserve practical access to simplified court procedures for low-value claims, while maintaining arbitration as the primary dispute resolution mechanism for larger or more complex matters.

Any appeal or further dispute resolution following a small claims judgment remains subject to the arbitration framework set forth in this agreement.

(j) Severability. If it is determined that any paragraph or provision in this arbitration clause is illegal, invalid, or unenforceable, such illegality, invalidity or unenforceability shall not affect the other paragraphs and provisions of this arbitration clause. The remainder of this arbitration clause shall continue in full force and effect as if the severed paragraph or provision had not been included. Notwithstanding this severability provision, if a court of competent jurisdiction determined paragraph G to be void, illegal, invalid or unenforceable the Parties agree that paragraph G above will be severed and that this arbitration clause shall be void in its entirety.

(k) Right to Opt Out. If BORROWER does not want this arbitration clause to apply, BORROWER may reject it by mailing a written notice to LENDER that lists BORROWER name, address and account number and states that BORROWER is opting out of the arbitration clause. An opt out notice is only effective if it is signed by BORROWER, and the envelope that the opt out notice is sent in is postmarked no more than 30 calendar days after the date BORROWER signs this Note. If BORROWER opts out of this arbitration clause, it will not affect any other provision of this Note or my obligations under the Note. BORROWER has the right to opt out of the arbitration clause in this Note by sending written notice to LENDER within the time and manner specified above. The notice must be timely and comply with all requirements set forth in this Note.

- If the opt-out is done correctly and on time: Arbitration will not apply to this Note.

- If the opt-out is done incorrectly or late: Arbitration will still apply, and the arbitration clause will be effective from the date of this Note.

This provision provides Borrower with a time-limited right to opt out of the arbitration agreement at the beginning of the lending relationship. Arbitration clauses are commonly used in consumer lending to establish a standardized method for resolving disputes outside of court; however, this provision allows Borrower to make an affirmative election to decline arbitration within a defined period after signing the Note.

The opt-out right is not inherently advantageous or disadvantageous to Borrower. Arbitration and court-based dispute resolution each have different procedural characteristics, and the choice primarily determines the forum in which disputes will be resolved rather than the underlying rights of the parties.

If properly exercised, the opt-out applies only to the arbitration provision and does not affect any other term of the Note. If not exercised within the specified timeframe, arbitration becomes the agreed method for dispute resolution under the terms of the agreement.

Why this provision exists

This clause exists less as a matter of legal necessity and more as a combination of consumer protection design and enforceability strategy in consumer lending agreements.

1. Voluntary agreement requirement

Arbitration is enforceable under U.S. contract law only if it is clearly disclosed, affirmatively agreed to, and not unconscionable. A time-limited opt-out helps demonstrate that the borrower had a meaningful choice at the time of contracting.

2. Reduces legal challenge risk

Courts are more likely to uphold arbitration provisions when the borrower had a clear and practical opportunity to reject them. The opt-out structure helps reduce claims that the clause was procedurally unfair or hidden.

3. Time-limited consumer election

This is a one-time decision window. It is not an ongoing right. Once the opt-out period expires (e.g., 30 days), arbitration becomes binding under the agreement.

4. Why it is often overlooked

In practice, this right is frequently missed because it is embedded in contract documents, requires affirmative written action, is time-sensitive, and is rarely exercised by borrowers.

Bottom line

This provision creates a structured, time-bound opportunity for the borrower to choose whether disputes will be resolved in court or through arbitration. It strengthens enforceability while preserving an early-stage consumer election right that must be actively exercised to be effective.

BORROWER acknowledges that any valid opt-out applies only to this Note and does not affect any other past, present, or future agreements with LENDER.

(i) FOR ALL DISPUTES COVERED BY THIS PROVISION, THE PARTIES HAVE AGREED TO WAIVE THEIR RIGHT TO A TRIAL BY JURY, THEIR RIGHT TO PARTICIPATE IN CLASS ACTIONS OR CLASS ARBITRATIONS, AND THEIR RIGHT TO SEEK PUNITIVE AND/OR EXEMPLARY DAMAGES. EXCEPT FOR DISPUTES AND CLAIMS NOT SUBJECT TO THIS PROVISION, ARBITRATION SHALL BE IN PLACE OF ANY CIVIL LITIGATION IN ANY COURT AND IN PLACE OF ANY TRIAL BY JURY.

THE TERMS OF THIS PROVISION AFFECT MY LEGAL RIGHTS. IF I DO NOT UNDERSTAND ANY TERMS OF THIS PROVISION OR THE COST, ADVANTAGES OR DISADVANTAGES OF ARBITRATION, I UNDERSTAND I SHOULD SEEK INDEPENDENT ADVICE BEFORE SIGNING THIS NOTE. BY SIGNING THIS NOTE I ACKNOWLEDGE THAT I HAVE READ, UNDERSTAND AND AGREE TO BE BOUND BY EACH OF THE PROVISIONS, COVENANTS AND STIPULATIONS SET FORTH ABOVE.

20.NO WARRANTIES; LIMITATION ON LIABILITY. EXCEPT AS EXPRESSLY SET FORTH IN THIS NOTE, BORROWER UNDERSTANDS LENDER HAS MADE NO REPRESENTATIONS OR WARRANTIES TO BORROWER, INCLUDING ANY IMPLIED WARRANTIES OF MERCHANTABILITY, OR FITNESS FOR A PARTICULAR PURPOSE. IN NO EVENT WILL LENDER BE LIABLE TO BORROWER FOR ANY LOST PROFITS OR SPECIAL, EXEMPLARY, CONSEQUENTIAL OR PUNITIVE DAMAGES, EVEN IF BORROWER INFORMS LENDER OF THE POSSIBILITY OF SUCH DAMAGES. FURTHERMORE, BORROWER UNDERSTANDS THAT LENDER MAKES NO REPRESENTATION OR WARRANTY TO BORROWER REGARDING THE EFFECT THAT THE NOTE MAY HAVE UPON BORROWER’S FOREIGN, FEDERAL, STATE OR LOCAL TAX LIABILITY.

21. Headings. The section and paragraph headings contained in this Agreement are for reference purposes only and shall not be deemed to limit, expand, or otherwise affect the meaning or interpretation of any provision of this Agreement.

22. Entire Agreement. The loan application and all loan disclosures are considered part of this Note and are incorporated by reference. This Note, together with the loan application and disclosures, represents the entire agreement between LENDER and BORROWER.

23. Miscellaneous. To the greatest extent not prohibited by applicable law, BORROWER is liable to LENDER for LENDER legal costs if LENDER refers collection of BORROWER’s loan to a lawyer who is not LENDER’S salaried employee. These costs may include reasonable attorneys’ fees as well as costs and expenses for any legal advice. If a law that applies to my loan and sets maximum loan charges is finally interpreted so that the interest or other loan charges collected or to be collected in connection with BORROWER loan exceed the permitted limits then: (a) any such loan charge will be reduced by the amount necessary to reduce the charge to the permitted limit and (b) any sums already collected from that exceeded permitted limits will be refunded to BORROWER. LENDER may choose to make this refund by reducing the principal BORROWER owes under the Note or by making a direct payment to BORROWER. No provision of this Note may be modified or limited except by a written agreement signed by both LENDER and BORROWER. The unenforceability of any provision of this Note will not affect the enforceability or validity of any other provision of law.

24. Covered Military Borrowers. If BORROWER is a “covered borrower” as defined under CFR section 232.3(g)(1), the Military Lending Act, 10 U.S.C. section 987 as amended, BORROWER agrees that (i) the provisions of Paragraph 15 (Disputes; Arbitration), (ii) any waiver of right to legal recourse under any state or federal law (including, but not limited to the waiver of defense under Section 7 and the waiver of presentment, notice of dishonor, protest and all other demands and notices otherwise applicable under Section 11) and (iii) any other provision in this Note that is not enforceable against me under the Military Lending Act, do not apply to me.

By signing this Note electronically BORROWER acknowledges that they (i) have read and understand all terms and conditions of this Note, (ii) agree to the terms set forth in this note, and (iii) acknowledge receipt of a copy of this Note that has no incomplete or blank word or data inputs where it appears there should be additional information such as words or numbers added. I understand this Note is executed in, and loan proceeds are distributed from, the state of Virginia.,

By ———————————- [Borrower Name]

————————————-[ Borrower signature ]

Date: